Recently I received a phone call from an old time friend. I was excited to hear her voice. We had a lot to discuss, from one point to another. From our discussion I realized she was having some concerns about cashflow, investment and general fear of unknown.

She pointed me to a man who throughout his entire career did not believe in keeping/saving money. Any amount more than N100,000 or N200,000 is put into investment especially real estate. But upon his retirement realized that the rental income from his tenants is heavily dependent on the state of the economy. And as his tenants struggle to pay, he is finding retirement challenging.

On the flip side of the coin is another man that believed in saving up all his income whilst in active service. Unfortunately at his demise the family struggled to claim the money from his bank.

The strongest fear that drives most of us is fear of the unknown, especially during our active years.

The oldest and strongest emotion of mankind is fear, and the oldest and strongest kind of fear is fear of the unknown (H.P Lovecraft)

I have seen many languish in retirement, waiting on their children to support them. Unfortunately many of these kids are victims of economy mismanagement and policy malfunctioning and few that managed to survive are so belabored financially that they soon end up in the same old cycle of pain and poverty.

This sends me thinking; What is the best approach to prepare for the off-cycle of life? How can one maintain a stable retirement life?

The finest of all human achievements and the most difficult – is merely being reasonable. (Anonymous)

Our deepest beliefs about money are formed at the early years of our development. School did not teach us about money and investment at an early age. Much like sex, the issue of money was left either to our parents who knew little about it or to us to figure out later in life.

So what is the best way to live and learn?

The truth is that there is no best way – only your way. What is important is to strike a balance.

Everyone needs to construct his or her portfolio in a way that serves your time horizon and controls your risk.

The way to approach financial planning at age 20yrs – 30yrs or as a single person is not the same way to approach money at age 30yrs – 45yrs and when married. And also as you enter age 45yrs to 55yrs your approach to money should change and in retirement age 55yrs – 65yrs and even beyond, your use of money would be different.

You should create a portfolio of investment that is aggressive while you are young and start moving position gradually towards conservative end as you get older.

Everyone needs to realize that their salaries and income from their trade is just what it is, INCOME.

It is dependent on your employer, and the economy. This already has a systemic risk built into it. And this risk is what manifests in the off cycle part of life, the pain cycle.

Naturally we are all aware of this, but many do not really prepare or understand how to hedge against this risk. Many depend on retirement benefits while others don’t even have that privilege.

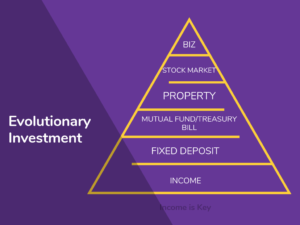

I am of the opinion that while actively working, everyone should have an evolutionary investment structure shown in the image below:

At the based is INCOME. A portion of this income should be saved up as available cash in Fixed Deposit Account with a moderate interest rate. Once the target is met, allow the interest to compound. There is power in compound interest.

Next segment is Mutual Fund and Treasure Bills, typically the money market.

Once the money market investment target is met, the next segment to move into is the property segment. Here you can invest in landed property or building with a view to cashing out your capital appreciation.

Once your base is set, the next segment is the Stock market.

You should understand that stock market in the long run tends to appreciate. Historically, stock market downward trend does not outlast the upward trend. So in effect, it will always move up, especially as productivity in the economy improves. So when investing, you need to take a long term view and invest in blue-chip companies with years of operation and track record.

It is important to have pension or redundancy insurance. If your employer has one for you, that is fantastic, otherwise you need to get one for yourself as soon as you are employed.

It is also important to have health insurance. And the moment you have a child, you will do well to treat him/her as an independent entity. Open a separate account for the child and ensure that you fund it regularly. You can also credit some of your investment returns into it.

You have to moderate your philanthropic gestures. Remember you are not the Alpha and the Omega. You cannot solve everyone’s problem. Let your investment return be what will serve you, your children and those that you want to assist, not your income. Your income is your capital for investment while you are actively working. And your investment will later become your Income when you are no longer working or active.